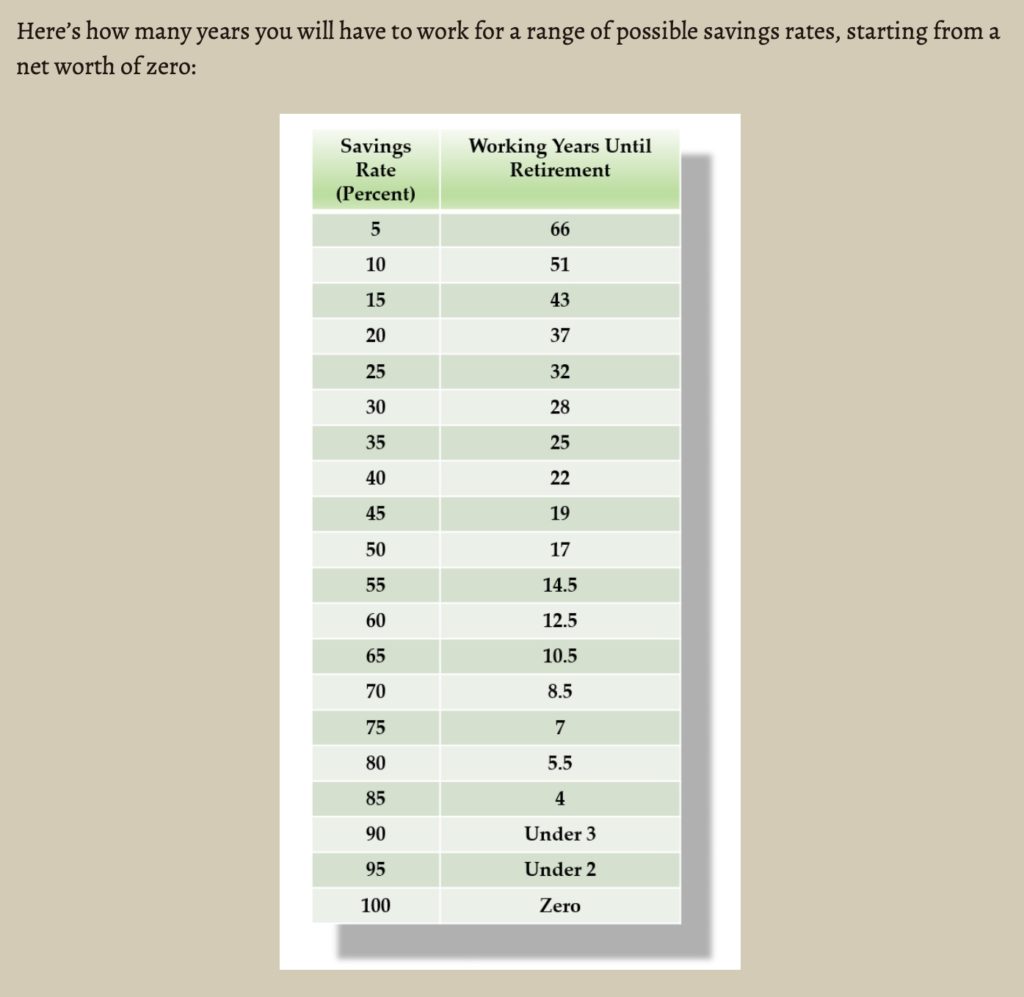

I keep this table from Mr. Money Moustache on my phone and look at it when I need a reminder about retirement options.

I have to be honest, for some reason I’ve never believed that I would make it to retirement age (only one of my grandparents lived longer than age 65) and so I’ve never REALLY planned for it. Yes, I have a retirement account through work and I qualify for a pension but I’ve never really paid attention to the exact numbers or path that effect your retirement age (or the age at which you can retire). However, I have a stressful job and when I think about doing said job until I am 67 (current US retirement age) I firmly believe that is impossible. I’d like to do something else and I am currently trying to figure out how to make that a reality.

This table represents a scale from worst case scenario to best case scenario. What I mean is, I am 46 years old and looking at the chart I can see that if I was truly starting from net zero and I only save 5% of my income I will never be able to retire and if I were somehow able to save 75% of my income I’d only have to do that for 7 years. I think most of us would be hard pressed to save 75% of our income but the chart allows us to see the outcome wherever we fall in between and allows us to see the difference that reaching the next level would make. For example, I’m at a 44% savings rate of my monthly income and I know the exact dollar amount I’d have to cut from my budget to make 50%. Finding places to cut that extra 6% is proving difficult but I can see from the chart if I can manage it, I’d be able to stop working a whole 2 years earlier. That’s why I like to look at this graphic. It shows that even if I was starting from zero, if I plan well, I could still retire early.

Steps I’ve taken to try and increase my savings rate:

- Put in extra hours and work to increase my salary. I have to admit that I’ve done the work (and put in the time) to raise my salary as much as is possible and so although Mr. Money Moustache claims he made it to early retirement on a normal salary, I’ve been poor enough to know that his previous (and my) 6 figure salary are not normal or average. I live in an expensive city and so salaries were increased to try and keep up with the cost of living (although if you look at the number of homeless people in the city, it’s clearly not working for everyone). In my case, the inflation rate in my city is 10% for the year but my salary was only increased 7%.

- Created a budget. Any good goal starts with a present level of performance. You can’t decide what a good realistic goal is or make changes unless you know where you currently are. I went back and looked at my spending for 3 months and then made an excel spreadsheet with the data. I recommend making one column that shows you how much your expenses are a month but also another column that shows the annual amount for each item. This helps see the true cost because when I think about something costing $11 a month I think that’s not much but when I realize that is $132 a year I might still feel it’s worth it but in some cases looking at the annual cost made me just say no, I can do without that. A budget also allows you to see what percentage of your income you are spending on different categories.

- Decided what items align with my values and cut the rest. In I Will Teach You to be Rich, Sethi points out it’s ok to spend money on things you value but if it’s not something you value, cut it out of your budget or go for the cheapest version you can find. For example, I value education and learning so I have a Kindle Unlimited subscription. I don’t value sitting around watching tv or movies so there is no cable or movie nights in my budget. Thinking about and developing values will help you budget appropriately and have money for the things that really matter to you.

- Thought outside the box to cut costs on some essential items. I’ve had AT&T cell service for 25 years. I just assumed my phone bill was at the going rate. I recently was going over my data allotment due to work meetings on my phone. I was thinking I needed to increase my data (and bill) because of it. However, my bill was so expensive as it was, I was balking at the idea of having to spend more. This led me to look around and discover the world of budget cell service. I was able to switch my service, get much more data (I looked at my old bills to see how much I needed) and cut my bill by 45%! (The two best I found were Mint Mobile and US Mobile. Cricket Mobile has an Affordable Connectivity Program for eligible customers with federal benefits. You can check carrier coverage at Coverage Critic). Another example is I stopped buying gas at my local gas station and started going a bit more out of the way to get my gas at Costco (the price difference is $1 a gallon and when your tank holds 35 gallons that’s a $35 extra savings a month.)

- Review my budget and spending often. I often can be found reviewing my Excel spreadsheet to see if I can cut costs anywhere or to review the effects of extra work on my savings account. Don’t beat yourself up over mishaps (spending an extra $10 at the grocery store) but do try and stick to your budget the best you can. Reviewing your spreadsheet can also remind you how much you can save if you stick with it and this can help keep you motivated. If you want to combine the ideas in this table with the specifics of your individual situation use this calculator to work that out. For me personally, the calculator gave me peace of mind that it will turn out in the end. My effort to increase my savings rate will just determine when I can retire vs. if I can retire.

One last thing to note about this table is it assumes that your return on investment rate is 5% after taxes (so 8% but only 5% after taxes are paid). If you can learn to do better than that with your investments, you are effectively cutting down on the number of years needed to retire.

Learn how to improve your investment strategy by reading my article Simple ETF Investing.